Ooh, the behavioral economists are going to be so smug about this.

Category: Tech news

hacking,system security,protection against hackers,tech-news,gadgets,gaming

Get Ready for Summer With These Nature-Themed Board Games

We selected a few great outdoorsy games that are perfect for playing on the patio or by an open window.

They Rage-Quit the School System—and They’re Not Going Back

The pandemic created a new, more diverse, more connected crop of homeschoolers. They could help shape what learning looks like for everyone.

The All-Seeing Eyes of New York’s 15,000 Surveillance Cameras

Video from the cameras is often used in facial-recognition searches. A report finds they are most common in neighborhoods with large nonwhite populations.

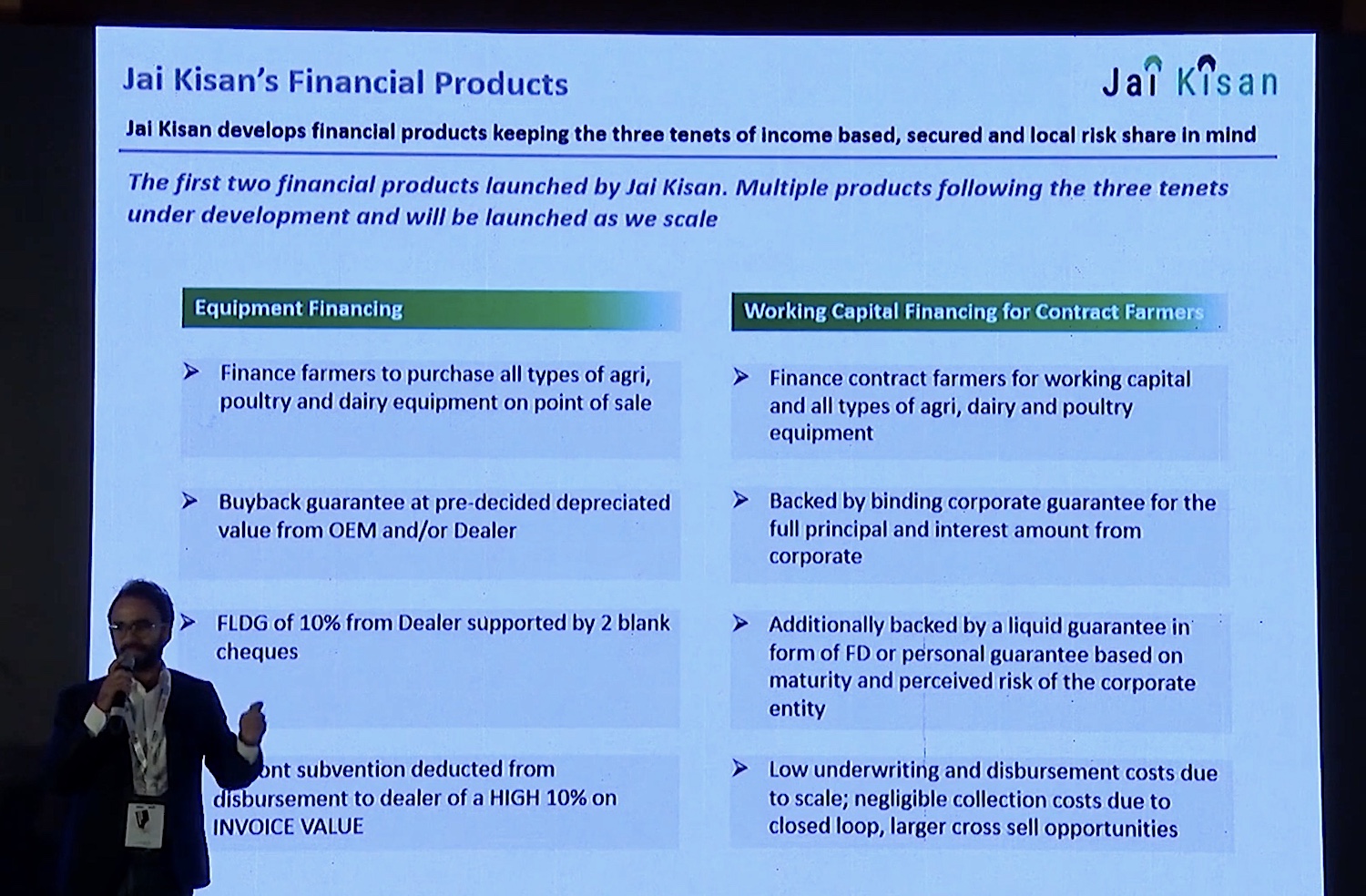

Jai Kisan, a fintech startup aimed at rural India, raises $30 million

Jai Kisan, an Indian startup that is attempting to bring financial services to rural India, where commercial banks have a single-digit penetration, said on Monday it has raised $30 million in a new financing round as it looks to scale its business.

Hundreds of millions of people in India today live in rural areas. Most of them don’t have a credit score. The professions they work on — largely farming — aren’t considered a business by most lenders in India. These farmers and other professionals also don’t have a documented credit history, which puts them in a risky category for banks to grant them a loan.

Much of the credit these people do raise ends up getting invested in unproductive usage, which leads to higher interest and default rates.

Three-year-old Mumbai-headquartered Jai Kisan is attempting to address this by treating farmers and other similar professionals as businesses instead of consumers.

The startup has developed its own system — which it calls Bharat Khata — that is helping individuals and businesses get access to cheaper financing and ensures that the money they raise is being used for agri-inputs and equipment and other income generating purposes and enablement of rural commerce transactions.

Arjun Ahluwalia, co-founder and chief executive of Jai Kisan, said financial services is crucial for these individuals as their entire economy depends on it. “The ability to buy now and pay later is how most people shop for things in India. Credit is an expectation by the Indian customer — it’s not a value added service,” he told TechCrunch in an interview.

“If there is availability of formal financing to customers, it’s not just customer who does well. The entire ecosystem that revolves around that customer benefits,” he said, pointing to the rise of Bajaj Finance, which has helped several businesses flourish in India by giving credit to customers at the time of purchase, and Xiaomi, India’s largest smartphone vendor, which sells a large number of its devices to customers on monthly instalment plans.

Ahluwalia at a conference in 2019 (India FinTech Forum)

Bharat Khata service, which was launched in April last year, captured more than $380 million of annualized GTV run-rate across over 25,000 storefronts by the financial year that ended in March this year, the startup said.

“Jai Kisan has financed over 15% of the transactions which portrays the monetizability and quality of commerce being captured. The ability to have visibility and virality of high-quality transactions has enabled Jai Kisan to scale business by over 50% in 3 months. The unprecedented growth trajectory stands testament to Jai Kisan’s capabilities to deploy capital efficiently by focusing on core customer credit needs,” the startup said.

The startup, which operates in eight Indian states in South India, is now looking to scale its presence across the country and also increase the headcount. On Monday, it said it had raised $30 million in a Series A round led by Mirae Asset, Syngenta Ventures, and existing investors Blume, Arkam Ventures, NABVENTURES, Prophetic Ventures and Better Capital.

An unspecified amount of the financing was raised as debt from Blacksoil, Stride Ventures, and Trifecta Capital.

“Jai Kisan is at the cusp of disrupting the rural financing industry and we’re glad to be a part of their growth story. Jai Kisan’s stellar growth, excellent asset quality and expanding footprint make them a highly differentiated player in the segment,” said Ashish Dave, chief executive of the India Venture Investments for the South Korean firm Mirae Asset.

“Mirae Asset has always believed in backing companies which aim to become category leaders which is evident from our other investments and we believe Jai Kisan is on the journey of doing so for rural finance,” he added.

Like most fintech startups, Jai Kisan has so far relied on its banking and other financial institutions to finance credit to businesses. The startup said it will now finance 20% of all loans by itself. Which is why it is also raising some money in debt in the new round.

21 Memorial Day Deals to Spruce Up Your Smart Home

From smart toothbrushes to app-controlled power strips, these deals will add a high-tech boost to your abode.

The Best Memorial Day Sales on Tech, Gaming, Home, and More

There are deals on the best streaming stick, our favorite sunglasses, and dozens of other WIRED top picks this holiday weekend.

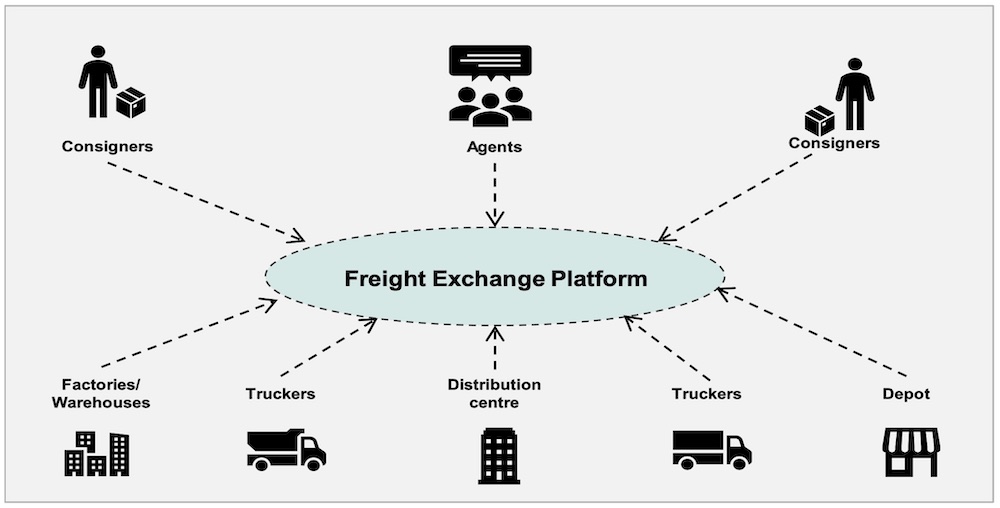

Indian logistics giant Delhivery raises $277 million ahead of IPO

Delhivery, India’s largest independent e-commerce logistics startup, has raised $277 million in what is expected to be the final funding round before the firm files for an IPO later this year.

In a regulatory filing, the Gurgaon-headquartered startup disclosed it had raised $277 million in a round led by Boston-headquartered investment firm Fidelity. Singapore’s sovereign wealth fund GIC, Abu Dhabi’s Chimera, and UK’s Baillie Gifford also participated in the new round, a name* of which the startup didn’t specify.

The new round valued the 10-year-old startup at about $3 billion. Delhivery — which also counts SoftBank Vision Fund, Tiger Global Management, Times Internet, The Carlyle Group, and Steadview Capital among its investors — has raised about $1.23 billion to date.

Delhivery began its life as a food delivery firm, but has since shifted to a full suite of logistics services in over 2,300 Indian cities and more than 17,500 zip codes.

It is among a handful of startups attempting to digitize the demand and supply system of the logistics market through a freight exchange platform.

Research and image: Bernstein

Its platform connects consigners, agents and truckers offering road transport solutions. The startup says the platform reduces the role of brokers, makes some of its assets such as trucking — the most popular transportation mode for Delhivery — more efficient, and ensures round the clock operations.

This digitization is crucial to address the inefficiencies in the Indian logistics industry that has long stunted the national economy. Poor planning and forecasting of demand and supply increases the carrying costs, theft, damages, and delays, analysts at Bernstein wrote in a report last month about India’s logistics market.

Delhivery, which says it has delivered over 1 billion orders, works with “all of India’s largest e-commerce companies and leading enterprises,” according to its website, where it also says the startup has worked with over 10,000 customers. For the last leg of the delivery, its couriers are assigned an area that never exceeds 2 sq km, allowing them to make several delivery runs a day to save time.

Indian logistics market’s TAM (total addressable market) is over $200 billion, Bernstein analysts said.

The startup said late last year that it was planning to invest over $40 million within two years to expand and increase its fleet size to meet the growing demand of orders as more people shop online amid the pandemic.

(*Indian news outlet Entrackr, which first reported on the filing, suggested it’s a Series H round. But according to insight platform Tracxn, there is no record of a Series G round for Delhivery. The startup didn’t comment on Sunday.)

For startups, trustworthy security means going above and beyond compliance standards

Oren Yunger

Contributor

Contributor

Oren Yunger is an investor at GGV Capital, where he leads the cybersecurity vertical and drives investments in enterprise IT, data infrastructure, and developer tools. He was previously chief information security officer at a SaaS company and a public financial institution.

When it comes to meeting compliance standards, many startups are dominating the alphabet. From GDPR and CCPA to SOC 2, ISO27001, PCI DSS and HIPAA, companies have been charging toward meeting the compliance standards required to operate their businesses.

Today, every healthcare founder knows their product must meet HIPAA compliance, and any company working in the consumer space would be well aware of GDPR, for example.

But a mistake many high-growth companies make is that they treat compliance as a catchall phrase that includes security. Thinking this could be an expensive and painful error. In reality, compliance means that a company meets a minimum set of controls. Security, on the other hand, encompasses a broad range of best practices and software that help address risks associated with the company’s operations.

It makes sense that startups want to tackle compliance first. Being compliant plays a big role in any company’s geographical expansion to regulated markets and in its penetration to new industries like finance or healthcare. So in many ways, achieving compliance is a part of a startup’s go-to-market kit. And indeed, enterprise buyers expect startups to check the compliance box before signing on as their customer, so startups are rightfully aligning around their buyers’ expectations.

One of the best ways startups can begin tackling security is with an early security hire.

With all of this in mind, it’s not surprising that we’ve witnessed a trend where startups achieve compliance from the very early days and often prioritize this motion over developing an exciting feature or launching a new campaign to bring in leads, for instance.

Compliance is an important milestone for a young company and one that moves the cybersecurity industry forward. It forces startup founders to put security hats on and think about protecting their company, as well as their customers. At the same time, compliance provides comfort to the enterprise buyer’s legal and security teams when engaging with emerging vendors. So why is compliance alone not enough?

First, compliance doesn’t mean security (although it is a step in the right direction). It is more often than not that young companies are compliant while being vulnerable in their security posture.

What does it look like? For example, a software company may have met SOC 2 standards that require all employees to install endpoint protection on their devices, but it may not have a way to enforce employees to actually activate and update the software. Furthermore, the company may lack a centrally managed tool for monitoring and reporting to see if any endpoint breaches have occurred, where, to whom and why. And, finally, the company may not have the expertise to quickly respond to and fix a data breach or attack.

Therefore, although compliance standards are met, several security flaws remain. The end result is that startups can suffer security breaches that end up costing them a bundle. For companies with under 500 employees, the average security breach costs an estimated $7.7 million, according to a study by IBM, not to mention the brand damage and lost trust from existing and potential customers.

Second, an unforeseen danger for startups is that compliance can create a false sense of safety. Receiving a compliance certificate from objective auditors and renowned organizations could give the impression that the security front is covered.

Once startups start gaining traction and signing upmarket customers, that sense of security grows, because if the startup managed to acquire security-minded customers from the F-500, being compliant must be enough for now and the startup is probably secure by association. When charging after enterprise deals, it’s the buyer’s expectations that push startups to achieve SOC 2 or ISO27001 compliance to satisfy the enterprise security threshold. But in many cases, enterprise buyers don’t ask sophisticated questions or go deeper into understanding the risk a vendor brings, so startups are never really called to task on their security systems.

Third, compliance only deals with a defined set of knowns. It doesn’t cover anything that is unknown and new since the last version of the regulatory requirements were written.

For example, APIs are growing in use, but regulations and compliance standards have yet to catch up with the trend. So an e-commerce company must be PCI-DSS compliant to accept credit card payments, but it may also leverage multiple APIs that have weak authentication or business logic flaws. When the PCI standard was written, APIs weren’t common, so they aren’t included in the regulations, yet now most fintech companies rely heavily on them. So a merchant may be PCI-DSS compliant, but use nonsecure APIs, potentially exposing customers to credit card breaches.

Startups are not to blame for the mix-up between compliance and security. It is difficult for any company to be both compliant and secure, and for startups with limited budget, time or security know-how, it’s especially challenging. In a perfect world, startups would be both compliant and secure from the get-go; it’s not realistic to expect early-stage companies to spend millions of dollars on bulletproofing their security infrastructure. But there are some things startups can do to become more secure.

One of the best ways startups can begin tackling security is with an early security hire. This team member might seem like a “nice to have” that you could put off until the company reaches a major headcount or revenue milestone, but I would argue that a head of security is a key early hire because this person’s job will be to focus entirely on analyzing threats and identifying, deploying and monitoring security practices. Additionally, startups would benefit from ensuring their technical teams are security-savvy and keep security top of mind when designing products and offerings.

Another tactic startups can take to bolster their security is to deploy the right tools. The good news is that startups can do so without breaking the bank; there are many security companies offering open-source, free or relatively affordable versions of their solutions for emerging companies to use, including Snyk, Auth0, HashiCorp, CrowdStrike and Cloudflare.

A full security rollout would include software and best practices for identity and access management, infrastructure, application development, resiliency and governance, but most startups are unlikely to have the time and budget necessary to deploy all pillars of a robust security infrastructure.

Luckily, there are resources like Security 4 Startups that offer a free, open-source framework for startups to figure out what to do first. The guide helps founders identify and solve the most common and important security challenges at every stage, providing a list of entry-level solutions as a solid start to building a long-term security program. In addition, compliance automation tools can help with continuous monitoring to ensure these controls stay in place.

For startups, compliance is critical for establishing trust with partners and customers. But if this trust is eroded after a security incident, it will be nearly impossible to regain it. Being secure, not only compliant, will help startups take trust to a whole other level and not only boost market momentum, but also make sure their products are here to stay.

So instead of equating compliance with security, I suggest expanding the equation to consider that compliance and security equal trust. And trust equals business success and longevity.

Chair Simulator Is a Game About … Sitting

The free PC game is pointless. That’s why it’s so absurdly fun.

Apple’s M1 Chip Has a Fascinating Flaw

The covert channel bug is harmless, but it demonstrates that even new CPUs have mistakes in them.

The 9 Best Portable Grills You Can Buy

We barbecued for weeks to find the right charcoal and propane gas grills for your home or that you can lug to the beach, park, or campsite.

Sleep Evolved Before Brains. Hydras Are Living Proof

Some of nature’s simplest animals suggest that sleep evolved long before centralized nervous systems.

6 Easy Ways to Make Your Own Memes

Your idea is destined to go viral. These sites and apps can help.

I’m a Cicada. You’re a Horny Human. We Are Not the Same

People preparing for a post-vax summer are likening themselves to the emerging insects. WIRED commissioned one cicada for its take.